🧗♂️ Building a strong credit profile before turning 20 is a powerful way to set yourself up for homeownership. Because mortgage lenders look for depth and stability in your credit history, starting early gives you a massive advantage.

To position yourself for a home purchase in East Tennessee, focus on these strategic steps to build a solid foundation.

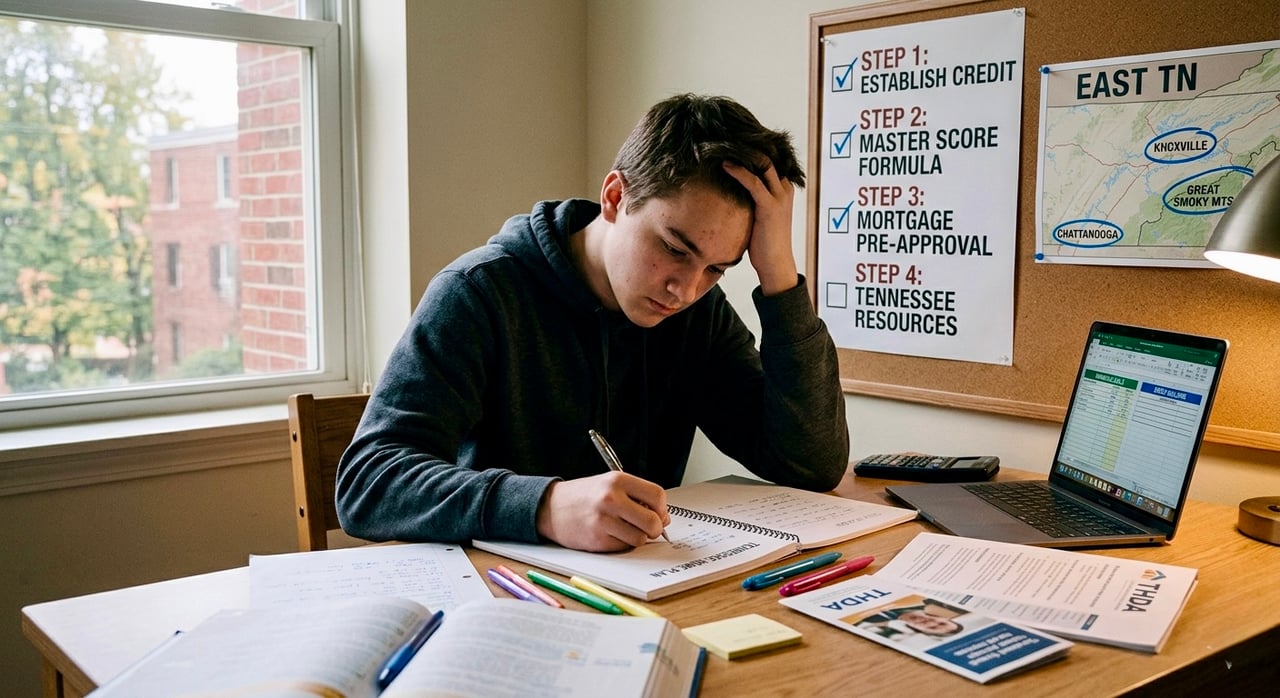

1. Establish Your First Credit Lines

If you have no credit history, you need to get accounts reporting to the three major credit bureaus (Equifax, Experian, and TransUnion).

Open a Secured Credit Card: If you cannot qualify for a standard unsecured card, a secured card is an excellent starter option. You provide a cash deposit (typically $200–$500), which becomes your credit limit. Use it for small, regular expenses like gas or groceries, and pay it off completely every month.

Become an Authorized User: If you have a trusted family member with an established credit card and a perfect payment history, ask to be added as an authorized user. Their good repayment history can report on your credit file, giving your score an immediate boost. Note: Ensure their card issuer reports authorized user data to the bureaus.

Consider a Credit Builder Loan: Offered by many local credit unions and banks, these loans do not give you money upfront. Instead, your monthly payments are held in a secured savings account while being reported to the credit bureaus as on time installment payments. Once paid off, the money is released to you, giving you both a credit boost and a small chunk of savings.

2. Master the Credit Score Formula

Lenders look closely at your FICO score. To maximize it, optimize the two heaviest components:

Payment History (35% of score): Never make a late payment. Set up automatic payments for at least the minimum balance, though paying the statement balance in full is ideal to avoid interest. A single 30 day late payment can drop a high score significantly and stay on your report for seven years.

Credit Utilization (30% of score): This is the percentage of your available credit that you use. Keep your total utilization below 10% to 30%. For example, if your credit card has a $500 limit, never let the statement balance cross $150. Paying your balance down before the monthly statement closing date keeps this number low.

3. Keep Mortgage Pre-Approval in Mind

Buying a home requires more than just a high credit score; it requires a profile that a mortgage underwriter trusts.

Build Length of Credit History: Length of history makes up 15% of your score. Lenders like to see accounts that have been open for at least 12 to 24 months. Keep your earliest accounts open and active; do not close them, as older accounts anchor your score.

Maintain Steady Income: Underwriters look for a stable, two year work history in a consistent field or a clear path from higher education into a career. Cash under the table or unverifiable income cannot be used to qualify for a mortgage.

Avoid New Credit Inquiries Before Applying: Within 6 to 12 months of planning to apply for a mortgage, stop opening new credit cards or taking out auto loans. Every hard inquiry can temporarily dip your score, and new open lines alter your debt to income (DTI) ratio.

4. Leverage Tennessee First Time Homebuyer Resources

As you plan for your purchase, keep an eye on regional requirements and state programs designed to help young buyers:

Aim for a 640+ Score: While some conventional or FHA loans accept lower, state sponsored programs in Tennessee generally require a minimum credit score of 640 to qualify for premium terms and assistance.

Explore THDA Loans: The Tennessee Housing Development Agency (THDA) offers the Great Choice Home Loan program, providing affordable, 30 year fixed rate mortgages to qualifying first time buyers.

Down Payment Assistance: Saving cash while under 20 can be tough. THDA also offers the Great Choice Plus program, which can provide second loans or deferred, forgivable options up to 5% of the purchase price to help cover your down payment and closing costs.

By keeping your utilization microscopic, automating your monthly payments, and building a verifiable employment history over the next couple of years, you will be in a prime position to secure a mortgage pre-approval when you are ready to shop the East Tennessee market.

Brandon Stitt

Top Agent - Proverbs 13:22 - Oak Ridge - Oliver Springs - Tennessee